A personal financial plan is imperative, especially if you are a Nigerian. You want to know why? Check the following statistics. In 1980, only 25% of Nigerians lived below the poverty line. It increased to 78% in 2007 and 89% in 2011. In the 70s, Nigeria was the 48th richest and most developed nation in the world. The country went to 178th in the 90s and is still struggling for freedom to date.

See Also: Poverty Is Not About Financial Challenges, It Is Of Improvised Mindsets

Additionally, in 2007, Nigeria became the 37th largest economy and one of the ten fastest-growing economies due to the oil boom and other factors yet Nigeria was 138th in the standard of living table and the 25th poorest nation in the world.

Are you beginning to think in my direction? The truth is, the challenges of most Nigerians are not a lack of source of income but a lack of financial literacy.

If everyone waits on the government for a change, we’ll wait forever. So, one of the best decisions you can make for yourself is to have a personal financial plan. A personal financial plan is key to being successful with your money.

Writing a personal financial plan is super simple and you’ll learn it in this article. However, note that when doing personal financial planning, there is no size fits all approach.

See Also: Financial Education 101: Should I Save Or Invest?

How To Write Your Personal Financial Plan

Step One: Determine Your Current Financial Status

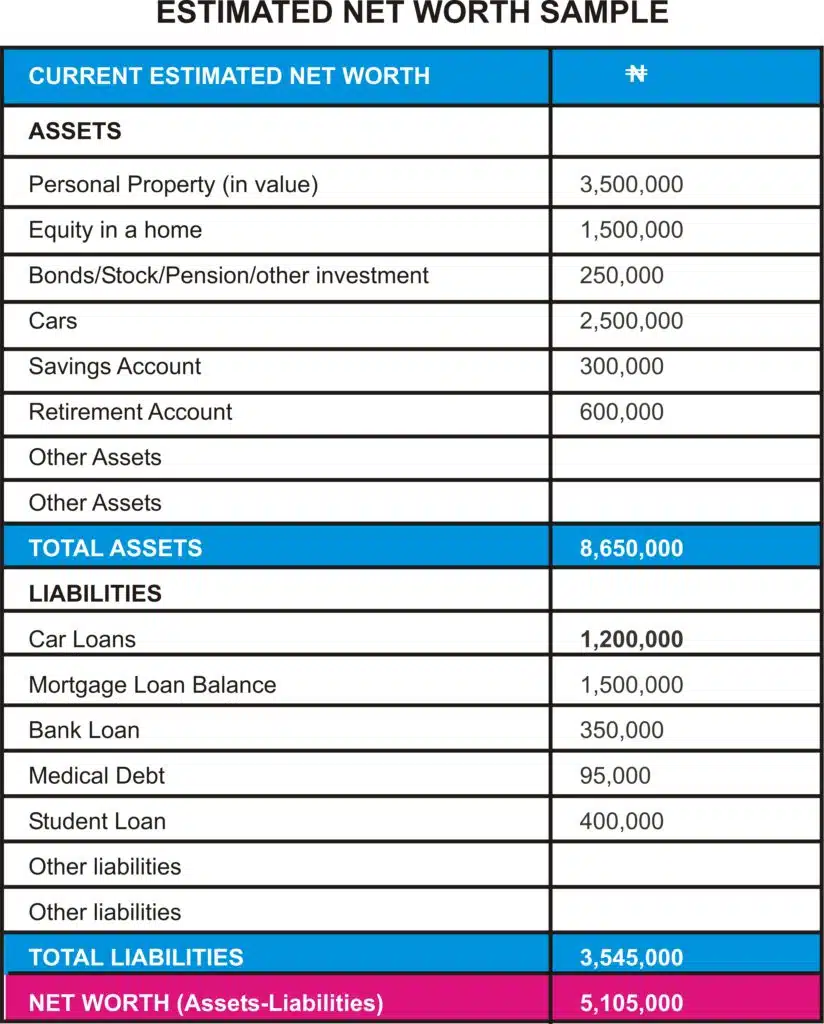

Before you write your personal financial plan, you need to know where you stand financially. Make a list of your current assets (the things you own) and liabilities (the things you owe).

Your assets include cash or cash equivalents; personal property, equity in a home, car, investments like bonds, stock and pensions. Liabilities on the other hand include your current bills and debts (car loans, student loans, medical debt, mortgage, bank loan, etc).

Thereafter, subtract your total liabilities from your total assets. The resulting number will give you your current net worth. If your current net worth is positive, it means that you have more assets than liabilities. If otherwise, you have more liabilities than assets which is not a good financial status.

See Also: What Is 401K?- Everything You Need to Know About 401K

See Also: How To Start Accounting Business In Nigeria

Step Two: Compile Your Financial Records

At this point, keep a record of your bank account statements, receipts, tax returns, insurance policy, bills, investment account statements, employee benefits statements and other documents related to your finances.

Also, it is expedient that you track your income and expenditures if you are determined to maintain a continuous personal financial plan. If you start documenting your cash flow, you will become more cautious of your spending.

See Also: Best Business Books For Entrepreneurs To Increase Their Hustle

Step Three: Set Goals For Your Financial Plan

Really, there is no financial plan without financial goals. If you don’t know where you are going, you won’t know when you get there. Determine what your short, intermediate and long term financial goals are. For instance, it could be to save N20,000 per month, so you can build your own home in some years to come. When setting your goal, make sure it is a SMART (specific, measurable, attainable, realistic, and time-based) goal.

Other common goals include:

- Vacation planning

- Wedding planning

- Debt elimination

- Family planning

- Postgraduate degree

- Starting a business

- Purchasing a car

- Saving for children’s education

- Settling your mortgage

- Paying for a professional course

- Saving for retirement

Another important factor to consider when doing a personal financial plan is to involve your family members or significant other in your plan. By involving them in your plan, you will be able to achieve your goals quickly because everyone will be on the same page with you.

You also need to outline the best way to utilise your current resources, increase your investments and savings. If your current source of income is not enough to help you achieve your financial goals, explore other ways to generate additional income. For example, you can explore online business ideas if you are in full-time employment or running just one business.

See Also: Achieving Our Developmental Goals Through Corporate Social Responsibility

Step Four: Implement Your Financial Action Plan

Once you’ve listed out your goals, and you’ve identified your sources of income, the next line of action is to consider your current situation and select which of the goals is appropriate to achieve first. Here are plans you should consider setting.

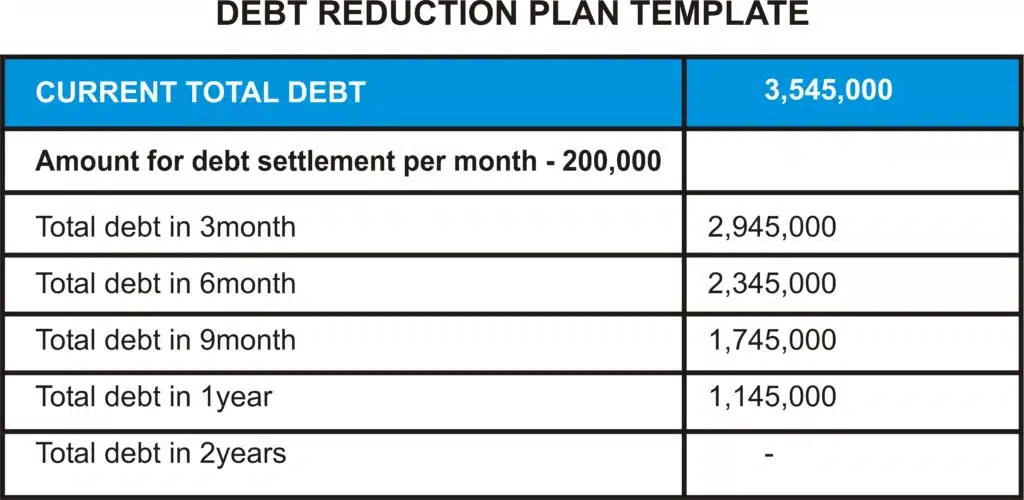

1. Pay Off Your Debt

Normally, many create personal financial plans to increase their net assets, which is a great intention. However, one of the greatest financial investments you can make is to pay off your debt. If you don’t do that, your debt will continually get in the way of your financial plan.

Allocate some resources monthly towards debt reduction and avoid increasing your debt. A good way to avoid debt is to live within your earnings.

See Also: Saving Money: 10 Tips On How To Save Money Every Month

2. Decide Which Financial Goal To Pursue First

In your early years of financial planning, it is important to focus on acquiring assets that will appreciate. Importantly, strive for a balanced approach toward short, medium and long term goals.

See Also: List Of Commercial Banks In Nigeria – Offerings And Overview.

3. Create A Budget

Budgeting plays a key role in the success of your financial plan. When you receive your income, follow the 70/30 rule. A maximum of 70% of your income should be spent on a budget. The remaining 30% can be split into two. A minimum of 10% of your income can be given to charity if you believe in giving back while the rest should go to savings and investment. Interestingly, several platforms can help you save and invest in today’s world.

Apart from that, you can invest in mutual funds, stocks, bonds, treasury bills, and cryptocurrency. The percentage of your savings and investment will be determined by your financial goal, so it can be tweaked as you deem fit.

To increase your savings, cut down on your expenses and increase your income. The most important thing is that you must create a monthly budget and stick with it. A good financial planner should not spend his/her income on something he/she cannot account for.

Creating a budget is a sign of financial responsibility and you’ll thank yourself for it in the long run. To achieve this, you can find a budgeting app that helps you automatically track your income and expenses. Some options include: Mint, Wally, and Personal Capital.

See Also: 15 Investing Apps And Websites For Entrepreneurs In Nigeria

Importantly, from the 70%, start an emergency fund that’ll help you deal with emergencies when they arise. Else, you will find yourself dipping your hands into your savings and investment which is detrimental to your financial future.

It is always advisable to save up to six months of living expenses in case of emergencies. If anything, the coronavirus pandemic is a big teacher that has taught many the importance of having emergency funds.

How To Prepare A Budget

i. Remove your savings and investment from your income

ii. Write down the balance as the amount available for spending

iii. Create an expense list

iv. Break the expense into fixed (things you can’t do without) and variable (things you need but can adjust and whose price varies).

v. Total your monthly income and monthly expenses. If you have a higher expense column than the income, adjust your expenses

vi. Review your budget monthly

See Also: How To Access CBN Covid-19 Relief Fund For Businesses

4. Get A Financial Adviser

Although you can manage your finances yourself, it is sometimes advantageous to have a neutral person lead you in ways to handle your finances. These professionals will assist you in sticking with your financial plans. More importantly, financial advisers will also put you through the best investment opportunities to choose from in order to avoid being scammed or losing your money.

See Also: Payroll Management Tips For Entrepreneurs And Small Business Owners

Step Five: Get The Right Insurance

I believe it’s not your will that you work hard to acquire wealth and an unforeseen circumstance comes to wipe it out. Actually, insurance serves as a backup plan that will protect your assets if unforeseen circumstances that require a huge amount of money occur.

Insurance coverage could include: health, life, home, auto, disability, business and the likes. Today, you can insure anything of importance. With adequate insurance in place, circumstances that would have been a disaster will only be an inconvenience for you and your family.

See Also: Lists of Licensed Insurance Companies in Nigeria- 50 NAICOM-Approved Insurers You Can Trust

Step Six: Review Your Financial Plan Frequently

Once you have your financial plan in place, it’s important to always review the plan and make necessary adjustments when you accomplish a goal or your goal changes. It’s advisable to review your financial plan at least every six months.

See Also: Personal Investment Opportunities For Small Business Owners

Step Seven: Stay True To Your Financial Plan

It will not be easy at first to adhere to the new standing rule over your finances but you must understand that financial independence requires a lot of discipline. Some days will be tough because it’s not in human nature to delay gratification but it’s always worth the effort. Avoid overspending and impulse buying. Before buying anything, ask yourself these questions:

- Do you really need it?

- Is the price right?

- Is there a substitute for it?

- Will its value increase?

- Is the timing right?

- Does it require expensive upkeep?

- Have you compared prices?

- Will it help you achieve your goals and purpose in life?

These and many more are the questions to consider before spending. As long as you have a strong WHY for maintaining a financial plan, you will not find it difficult to stick with your game plan.

See Also: Mindset Shifts For Entrepreneurs To Make In Order To Achieve Their Goals.

How To Review Your Financial Plan

i. Fix A Date And Time

Allocate a particular date and time to go over your finances. Preferably, set a reminder on your calendar to help you remember your schedule.

ii. Reconcile Your Bank Statements With Your Financial Transactions

Every bank sends monthly bank statements to their customer’s email. So, print out your bank statements and check them against your spending for the past months. Also, check if you spend within your budget.

See Also: How To Get Loan From Development Bank Of Nigeria And Grow Your Business

iii. Review Your Financial Goals

The next thing to do is to check the financial goals you’ve met and cross them off your goal. You can set new goals or review other pending goals on your list.

iv. Follow Up On Your Savings And Investment

If you’ve automated your investment and savings, check to see the progress and the accumulated interest. Review your overall investment and plan to diversify where necessary. If you are maintaining a retirement account, check the progress as well.

See Also: Top 10 Mobile Loan Apps In Nigeria Where Employees And Entrepreneurs Can Access Loans

v. Check Your Net-Worth

The goal of a financial plan is to increase your net worth and you must keep track of it. When you clear your debt, your net worth will begin to increase. Don’t worry if you started out with a negative balance. As you stay consistent with your financial plan, that will change over time.

Important Questions To Ask When Reviewing Your Financial Plan

- Did I spend in line with my budget?

- Did I take steps that brought me closer to achieving my financial goals in the past months?

- What financial errors did I commit? And why did I make these errors?

- Was my spending in line with my core values?

- Am I saving enough to cover my long term financial plans?

- Do I have enough financial plans in place for my children?

- Are my investments enough or do I need to diversify?

- What expenses can I do without in the coming months that’ll help me save more?

- What big expenses am I incurring soon?

- How can I increase my source of income?

See Also: Most In-Demand Freelance Skills To Start And Earn Money

Don’t just ask yourself these questions, write down the answers in a book and go over them at intervals to be reminded to take the steps you’ve written down.

In conclusion, the journey of financial independence starts with a strong personal financial plan. The advantage of maintaining a financial plan far outweighs the disadvantages, so the best time to start is now.

There you have it. Are you currently maintaining a financial plan? Share your progress with us in the comment. More importantly, share this content with your audience if you found it useful.

Dear entrepreneur, gone are the days when social media is enough to push your brand. Today, you need a reputable site to mention and put you on the world map. This is what we offer you at entrepreneurs. ng. Reach out to us today to tell your story.

Best of luck!

To keep track of our activities, follow us on Instagram